Finance roles are often misunderstood—especially in growing businesses. It’s common for founders to blur the lines between a Controller and a Chief Financial Officer (CFO), assuming they’re just different labels for the same function. But this misconception can quietly hold a business back. While both roles are essential to financial health, they serve very different purposes, require distinct mindsets, and most importantly—drive very different outcomes.

Getting this right isn’t about semantics—it’s about strategy. Hiring a Controller when you really need a CFO means optimising for control instead of growth. And the reverse—expecting a CFO to manage day-to-day accounting—wastes resources and dilutes impact. Let’s unpack the real differences between these two critical roles, when you need each, and how hiring the right person at the right time can transform your business from financially functional to financially powerful.

Understanding the Role of a Controller

A Controller is the backbone of your internal finance function. Their role is primarily operational—focused on maintaining accurate financial records, ensuring compliance, managing reporting, and enforcing internal controls. They make sure the numbers are clean, the processes are tight, and the business stays on track with regulatory requirements. In short, they keep the house in order.

Controllers are detail-oriented doers. They’re fluent in accounting standards, comfortable with spreadsheets and ERP systems, and excellent at spotting discrepancies before they become problems. Their priority is accuracy and discipline, not commercial strategy. If your business needs someone to run payroll, close the books, manage invoices, and prepare monthly reports, a Controller is the right fit. But if you’re expecting them to guide high-level decisions or lead your growth plan—you’re likely expecting too much from the wrong role.

Understanding the Role of a CFO

A Chief Financial Officer (CFO) operates on an entirely different level. Their role is not about looking backwards—it’s about looking ahead. A CFO provides strategic financial leadership, helping the business make informed, data-backed decisions that support sustainable growth and long-term value creation. While they understand the numbers, their real power lies in knowing what to do with them.

A strong CFO—whether full-time or fractional—will focus on forecasting, scenario planning, investment strategy, and working capital optimisation. They work hand-in-hand with leadership teams across the business, aligning financial strategy with commercial objectives. From marketing campaigns to sales hires, from funding rounds to CAPEX planning, the CFO plays a key role in prioritising what will drive the highest return with the lowest risk. They don’t just manage costs—they help the business scale with confidence.

Why Mindset Matters: The Growth Enabler (CFO) vs. the Gatekeeper (FC)

The biggest difference between a Controller and a CFO isn’t just what they do—it’s how they think. A Controller’s mindset is rooted in protection: safeguarding the business through accuracy, compliance, and cost control. They’re there to maintain order, keep things tidy, and ensure nothing slips through the cracks. That’s incredibly valuable—but when it becomes the dominant voice in a growing business, it can unintentionally hold the company back.

A CFO’s mindset is geared towards growth. Their default is not “How do we cut costs?” but “Where should we invest for the best return?” They embrace calculated risk, advocate for strategic spending, and help leadership prioritise initiatives that will drive real commercial impact. Where a Controller might be inclined to say “no” to preserve the budget, a CFO asks “how” to make the numbers work for the opportunity ahead. That shift in perspective—from guarding the business to growing it—is what separates operational finance from strategic finance.

The Ideal Timeline: When to Hire Each One

The timing of when to bring in a Controller versus a CFO can make a significant difference in how efficiently—and how confidently—your business scales. It’s not just about the size of your business, but about its complexity and ambition.

As soon as your business starts to gain traction, you’ll need someone who can keep your financial house in order. This is when a Controller or strong finance manager should come in. They’ll ensure that bookkeeping is clean, data is timely, and reporting is accurate—because without a solid foundation, even the best strategy will fall apart. And no, outsourcing bookkeeping to an accountancy practice isn’t enough. Bookkeeping isn’t just about compliance—it’s about building trust in your numbers so you can use them to make informed decisions.

Once you pass the €1M revenue mark and you have serious growth aspirations, that’s when you should consider bringing in a fractional CFO. Even on a part-time basis, a CFO can instantly add strategic value, helping you with financial planning, capital allocation, working capital optimisation, and guiding big-picture decisions. It’s one of the smartest investments a scaling business can make—long before you’re ready to hire a full-time CFO.

Can One Person Do Both Jobs?

In theory, yes. In practice? Rarely—at least not effectively. While it might seem efficient to hire one person to handle both the financial operations and strategic planning, the reality is that Controller and CFO roles demand completely different skill sets and mindsets. Expecting one person to excel at both can result in one of two outcomes: overstretching a strategic leader with administrative tasks, or relying on an operational manager for high-level financial decisions they’re not equipped to make.

For early-stage businesses, a more sustainable (and cost-effective) structure is to have an in-house Controller managing the day-to-day finance function, while engaging a fractional CFO to lead on strategy. The Controller ensures data integrity, process discipline, and compliance. The fractional CFO brings experience, commercial insight, and future-facing leadership. Together, they form a finance function that is both solid at the core and sharp at the edge—able to maintain control while pursuing growth.

Real-World Impact: What Happens When You Get It Right (or Wrong)

Hiring the wrong financial role for your stage of growth can quietly stall your progress. One common mistake? Hiring a Controller and expecting them to act like a CFO. What often happens next is predictable: strategic decisions are delayed, growth opportunities are missed, and the business becomes focused on maintaining the status quo instead of pushing forward. The result? A financially compliant company that’s structurally sound—but strategically stuck.

On the flip side, when you get the mix right, the results are transformative. We’ve seen it first-hand at Quantro. In one case, a business with no financial visibility was making decisions purely on gut. Once we implemented a live dashboard with dynamic KPIs and paired it with strategic guidance, they saw 297% revenue growth, a 200%+ profit increase, and doubled their cash on hand—all within 18 months. That growth didn’t come from cutting costs. It came from using finance to unlock smarter, faster decisions.

Two Roles, One Goal – Smarter Growth

A Controller and a CFO serve very different purposes—but together, they provide the foundation and fuel for sustainable growth. The Controller ensures the business is built on accurate, timely financial data and solid internal processes. The CFO takes that foundation and uses it to drive the business forward—allocating capital strategically, guiding decision-making, and positioning the company for scale.

Understanding the difference isn’t just helpful—it’s essential. Hire a Controller when you need control. Hire a CFO when you want growth. Get both in place at the right time, and you turn finance from a support function into a strategic advantage. At GrowthCFO, we help businesses build that kind of financial leadership—fit for scale, built for results.

Cash flow forecasting isn’t just a financial hygiene habit — it’s a strategic tool.

Many founders believe that so long as the monthly budget balances, they’re on solid footing. But business doesn’t move monthly — it moves weekly (even daily in some very fast pace industries). Suppliers get nervous on Tuesday, not at month-end. A cash shortfall on week 9 won’t show up on your P&L until it’s too late.

This is why we build and maintain a 13-week rolling cash flow plan with every Quantro client — regardless of whether they’re flush with funding or tightening belts. It gives us time to see the issues coming, space to act, and the confidence to grab opportunities that short-term cash control makes possible.

Whether you're running a real estate development cycle, a SaaS startup burning investor cash, or a scaling agency juggling payroll and pipeline, a 13-week view gives you clarity today — not regret tomorrow.

What Is a 13-Week Cash Flow Forecast?

At its core, a 13-week cash flow forecast is a short-term, rolling view of your expected cash inflows and outflows, updated weekly. Rather than thinking in months or quarters, this tool lets you plan your business’s financial reality on a week-by-week basis for the next 3 months.

You’re not just looking at profit or loss (which doesn’t include VAT element init). You’re looking at actual cash movement: when invoices are expected to land, when suppliers will demand payment, when VAT is due, when salaries hit the bank. It’s granular. It’s live. And it’s actionable.

Unlike static monthly budgets, the 13-week model forces founders to connect daily decisions with immediate cash impact. It’s not about forecasting perfectly — it’s about being directionally correct and having time to act. Each week, you roll it forward one week, incorporating the latest receivables, payables, and any adjustments in timing.

It becomes your cash radar — and in business, visibility is everything.

Why It’s Not Just for Cash-Strapped Companies

There’s a myth that cash flow forecasting is only useful when things go wrong. In reality, a 13-week forecast is equally powerful when things are going right.

For funded companies — especially in SaaS or product-based startups — the 13-week view gives clarity on burn rate and runway. It answers key questions like: Can we afford to hire next month? When do we need the next funding round? Are we spending ahead of plan? It brings discipline without limiting ambition.

For fast-growing companies, this level of visibility enables better strategic timing. Let’s say you want to invest in new inventory, equipment, or marketing — the weekly forecast tells you when you’ll have the cash, or whether you can restructure payments to make it work. And for businesses that are cash-rich? That’s when timing matters most — using excess liquidity to negotiate better supplier terms, prepay obligations, or even capitalise on competitor weakness.

Even distressed businesses benefit: if you’re facing tight cash, the 13-week model buys time and shows you your levers— whether it’s delaying a non-critical expense, accelerating collections, or securing a short-term facility before the squeeze becomes existential.

In short, every business has something to gain from knowing what the next 90 days look like — not just where the year is going.

Real Outcomes from Clients Who Use It

At Quantro, we’ve seen first-hand how a 13-week cash flow plan turns uncertainty into opportunity. Here are two real cases from our own clients:

🟢 Case 1: Securing funding before the storm hit

One of our clients was showing strong revenue, but our 13-week forecast spotted a looming cash gap — still eight weeks away. Because we saw it early, we were able to prepare financials, speak to lenders, and secure a loan before the situation became urgent. The result? The client got better terms, faster approval, and avoided the classic last-minute financing panic that often leads to higher costs or missed opportunities.

🟢 Case 2: Using surplus cash to negotiate better terms

In another case, a client had a healthier-than-expected cash position. Most businesses would sit on that buffer. But because we had full visibility through the 13-week model, we analysed the opportunity cost of idle cash and realised we could negotiate early payment discounts. We approached a key supplier and secured a 7% discount by paying in advance — a decision that wouldn’t have been made without that week-level confidence in available cash.

These aren’t dramatic turnaround stories. They’re strategic wins — and that’s the point. Cash flow visibility isn't just about survival. It's about timing, leverage, and control.

What We Track Weekly and How We Automate It

The power of a 13-week forecast comes from its rhythm — but the effectiveness lies in what you track and how reliably you update it.

At Quantro, we build every 13-week cash flow model starting with a detailed budget. That gives us the “ideal case.” From there, we track and adjust weekly based on actual activity, not assumptions. Here’s what we focus on every single week:

✅ Accounts Receivable

We break AR down into four buckets:

0–30 days overdue

31–60

61–90

Over 90 days

Each one has its own strategy. Recent invoices might just need reminders. Older ones might require escalation or factoring. Crucially, if key receivables don’t land, we don’t make corresponding payments — simple but powerful logic that keeps control centralised.

✅ Accounts Payable

We track weekly obligations and match them to realistic inflows. No auto-payments unless cash is available. This weekly discipline prevents cascading issues like overdrafts or missed salaries.

✅ Tax, VAT, and Payroll

We include all non-negotiables — VAT filings, tax prepayments, salary cycles. These are often forgotten until it’s too late, but in our model they’re always visible.

✅ Automation & Structure

Once the budget is in place, we automate the full structure:

Weekly cash flow rolls forward

VAT and tax dates are auto-calculated

All changes link back to expected budget vs actuals This creates a system that doesn’t rely on memory, guesswork, or heroic spreadsheet manipulation every Sunday night.

On top of that we build hypotheses, where you can add costs or revenue and that will be illustrated automatically in both the budget and the cash flow.

We built this for our clients at Quantro so they never ask “how much cash do we have left?” — they already know, and more importantly, they know when they’ll need more.

What Founders Struggle With (and How to Overcome It)

Most founders don’t resist cash flow forecasting because they think it’s a bad idea — they resist it because they’ve experienced it as a manual, clunky process that’s always out of date.

Here are the most common challenges we see:

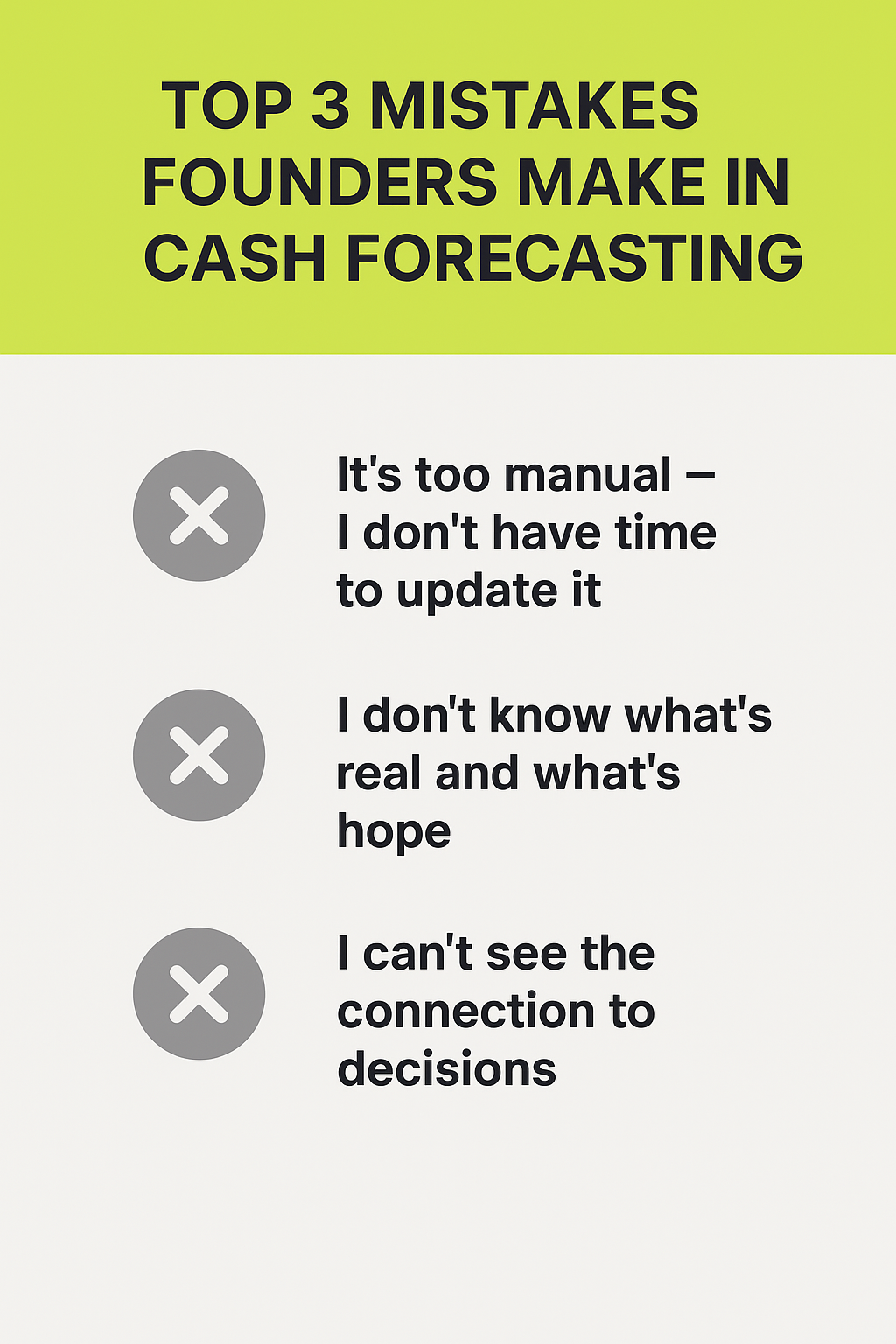

❌ “It’s too manual – I don’t have time to update it.”

Without structure, weekly forecasting turns into spreadsheet chaos. People rely on static files, copy-paste errors, and best guesses. That’s why we always start from a budget — not a blank page — and build automation on top.

❌ “I don’t know what’s real and what’s hope.”

Founders often mix up confirmed cash inflows with expected ones. That’s why we track AR in aged buckets and only count cash we’re confident in. You need to know the difference between “booked revenue” and “actual cash next Tuesday.”

❌ “I can’t see the connection to decisions.”

Even when founders have a cash forecast, they don’t link it to strategy. Should you hire? Buy inventory? Delay a payment? Cash flow tools must inform decision-making, not just compliance reporting.

The fix isn’t more accounting — it’s smarter financial design. When done right, a 13-week forecast runs in the background, alerts you before trouble, and empowers you before action.

Conclusion

In business, cash doesn’t move monthly — it moves weekly. And yet too many founders fly blind with outdated, static views of their finances. A 13-week cash flow forecast isn’t just a defensive tool for distressed companies — it’s a strategic system for every business, at any stage.

Whether you're managing a burn rate, expanding into new projects, or negotiating supplier terms, clarity over the next 90 days empowers better decisions today. It protects you from the downside and positions you to seize upside. It replaces panic with planning.

At Quantro, we believe every founder should know exactly when they’ll run out of cash — and exactly what to do before they get there. Weekly forecasting doesn’t just show you what’s coming. It gives you time to do something about it. Want to implement a 13-week cash forecast for your business? Let’s build it together.

Starting a business is a big adventure. It begins with a small idea – a seed – and grows over time through different stages. Each stage of a startup's growth is important and comes with its own challenges, especially regarding money. From the very beginning (Seed stage) to later stages (like Series C), businesses need to be smart about how they use their money to grow bigger and stronger. This isn't just about getting enough money to keep going; it's about making the right choices that will help the business succeed in the long run.

Knowing how to handle your business's finances is super important. It's not just about keeping track of what you spend and earn; it's also about telling a story that investors will believe in, finding the best ways to make your product or service popular, and making smart choices that help your business grow in the right direction. This guide is here to help companies understand how to face money challenges at each step of their growth. We'll share tips and tricks on how to manage money from the very start all the way to later stages of growth.

The Seed Stage – Laying the Foundations

At the start of any business, the Seed stage is where all begin. This stage is all about turning your big idea into something real that can attract more support. You need to validate your idea in the market, create your MVP, test it and find if there is a product-market fit. But in order to achieve all that, you need some resources to get going. For businesses, this means money to develop your product, do research, and find the right people to join your team.

Getting money at this stage has changed a lot. Nowadays, even the first bit of money you get can be quite big, more like what businesses used to get a decade ago when they were a bit more grown-up. This big start can be great, but it also means you have to be really careful about how you use it. You need to make sure you're spending on things that really help your business grow and not just burning money.

You need to figure out where to spend your first bits of money so you can develop your product and get people excited about it without wasting huge resources. This careful planning in the Seed stage sets the foundation for everything that comes next, making sure your business is ready to grow strong and healthy, but also to successfully land its Series A, where many businesses have failed to do so.

The Leap from Seed to Series A: Mastering the Transition

The transition from Seed to Series A is a pivotal moment in a startup's life cycle, marking a shift from proving a concept to proving the business can scale. This stage is less about the initial excitement of launching and more about demonstrating substantial progress and potential for significant growth. Achieving Series A funding signifies that a startup has successfully navigated the initial challenges of market entry and is now ready to scale its operations, product development, and market reach.

To stand out and secure Series A investment, startups must present a compelling case to investors that goes beyond the innovative idea or product. This involves showcasing a proven product-market fit, a scalable business model, and a clear strategy for revenue generation. A strong focus on key performance indicators (KPIs), such as customer acquisition costs (CAC), lifetime value (LTV) of a customer, and monthly recurring revenue (MRR), is crucial. These metrics not only demonstrate the startup's current success but also forecast its future growth potential.

Incorporating a financial expert or a fractional CFO at this stage can be a game-changer for startups. These professionals can provide strategic financial guidance, help in fine-tuning the business model, and prepare the startup for the rigorous due diligence process of Series A funding. They play a critical role in building a financial roadmap that outlines how the startup plans to achieve its growth objectives, manage cash flow efficiently, and optimise operational costs for scaling.

Successfully navigating the Seed to Series A transition requires a delicate balance between rapid growth and the development of a sustainable, scalable business model. Startups need to be agile, continuously adapting their strategies based on market feedback while maintaining a clear focus on long-term goals. This strategic approach not only positions startups favorably for Series A funding but also lays a solid foundation for future growth stages.

Scaling Up: Navigating the Series A to Series B Journey

The journey from Series A to Series B is marked by the need to scale operations, refine the product, and expand market presence. This phase is critical for startups, as it requires not just growth but sustainable and efficient growth. The focus shifts from simply proving a concept to demonstrating the ability to execute on a larger scale, attracting further investment for expansion.

For startups aiming to secure Series B funding, the emphasis is on showing strong customer traction, an expanding user base, and the scalability of the business model. Investors at this stage are looking for evidence that the startup can not only attract customers but also retain them over time, thereby increasing the lifetime value (LTV) and reducing the customer acquisition cost (CAC) in a way that promises long-term profitability.

Operational efficiency becomes paramount. Startups must optimise their operations to support growth without compromising quality or customer satisfaction. This might involve investing in technology, hiring talent, and refining internal processes to improve efficiency and productivity. The goal is to build a robust operational framework supporting accelerated growth and expansion into new markets or segments.

Financial metrics and modeling take center stage. At this point, startups must have clear visibility into their financial health and trajectory. This includes having a solid grasp of key financial metrics such as burn rate, gross margin, unit of economics and EBITDA. A comprehensive financial model that projects future growth and scalability is essential to convince investors of the startup's potential for success at the Series B stage and beyond.

Navigating the transition from Series A to Series B requires a strategic approach focused on growth, efficiency, and financial acumen. By demonstrating a scalable business model, operational excellence, and a clear path to profitability, startups can successfully secure Series B funding and position themselves for the next phase of growth.

Navigating Series B to Series C – Scaling for International Growth and Operational Excellence

As startups transition from Series B to Series C funding, the focus intensifies on scaling operations for international growth and achieving operational excellence. This stage is about leveraging the foundation built in earlier phases to expand aggressively into new markets and refine business operations for peak efficiency.

The move towards international growth requires a strategic approach, considering cultural nuances, regulatory environments, and market-specific consumer behaviours. Startups must conduct thorough market research to identify the most promising regions for expansion and tailor their product offerings and marketing strategies to meet local needs. This step not only broadens the customer base but also diversifies revenue streams, making the business more resilient to regional economic fluctuations.

Operational excellence becomes paramount as startups scale. This involves streamlining processes, implementing best practices in every department, and adopting advanced technologies to enhance productivity and reduce costs. Efficient operations support rapid scaling by ensuring that growth does not compromise product quality or customer satisfaction. Furthermore, a focus on operational excellence helps startups optimise their cash flow and extend their runway, making them more attractive to investors looking for businesses with tight control over their finances.

At the Series C stage, startups are expected to present solid financial metrics that indicate a clear path to profitability, if not profitability itself. This includes demonstrating strong unit economics, a sustainable growth rate, and effective management of operating expenses. Investors at this stage are particularly interested in seeing how startups plan to use additional funds to fuel growth without eroding profitability.

The journey from Series B to Series C is characterised by the startup's ability to execute expansion plans while maintaining a tight grip on operational efficiency and financial health. Success in this phase is marked by a startup's ability to operate at a global scale, demonstrating that its business model can thrive across diverse markets and withstand the challenges of scaling operations internationally.

Mastering Series C and Beyond: Preparing for Maturity and Market Leadership

At the Series C stage, startups are on the brink of major expansion or even preparing for public offering. This phase is about leveraging existing successes to secure a dominant market position and ensure financial sustainability. The focus shifts towards strategic planning fro growth, operational efficiency, and exploring paths like IPOs or acquisitions.

Success now depends on outmaneuvering competitors and solidifying the company's market presence. This could mean expanding product lines, entering new markets, or acquiring complementary businesses. The goal is to enhance the brand and deepen customer loyalty.

Financially, companies must show profitability, strong cash flow, and efficient use of capital. Preparing for an IPO or attracting acquisition offers required rigorous financial discipline and transparency. Startups must balance growth with financial health to attract further investment or prepare for public markets.

Wrapping Up the Startup Journey

The journey from seed to Series C is a pivotal path for startups, marked by growth, challenges, and strategic milestones. Initially, securing seed funding is all about validating the business idea and beginning to carve out a market presence. As startups evolve to the Series A and B stages, the focus shifts to proving the business model, scaling operations, and refining the product-market fit. By the time they reach Series C, startups are preparing for significant expansion, operational scaling, or exploring exit strategies.

Throughout this financial roadmap, the constant theme is the need for startups to adapt, strategise, and manage their finances smartly. Success lies in balancing innovation with strategic financial planning, ensuring the startup not only grows but thrives.

When seeking investment, you’re not just selling your idea—you’re selling confidence in that idea. Investors need to believe your business has the structure, strategy, and foresight to grow successfully. While a compelling vision is essential, the underlying data and financial discipline will give investors the confidence they need to commit. This is where your finance team steps in and can drive the investment.

A strong finance team acts as the bridge between vision and reality. They ensure that your forecasts are more than just numbers on a page; they’re grounded in solid data, reflect achievable milestones, and tell a credible story about your business’s future.

By focusing on internal and external metrics, your finance team helps turn your goals into a roadmap investors can trust. Finance drives investment and instil the confidence needed to attract and secure capital for growth.

Establishing Credibility Through Data-Driven Financial Forecasts

When it comes to securing investment, one of the first things investors look for is whether your financial forecasts are grounded in reality.

A robust financial forecast doesn’t just demonstrate projected revenue growth; it provides the reassurance that these figures are achievable. Your finance team is pivotal in ensuring your projections are ambitious and credible. But how do you strike that balance? The answer lies in data from within your company and the broader market.

Example of e-comm business

Start by benchmarking against similar companies. This involves identifying businesses that operate within the same industry, have similar strategies, and are in comparable geographic markets.

You can set challenging yet realistic targets by analysing what those companies have accomplished—particularly in areas such as paid media and organic growth.

In addition to external data, it is crucial to track your own performance. Your finance team should understand how your marketing and sales efforts convert into revenue and whether those conversion rates can be scaled.

By combining this internal and external data, your finance team can create financial forecasts demonstrating ambition and inspiring confidence. Investors will see that your projections are not just optimistic but achievable and grounded in well-supported analysis.

Addressing Financial Risk with a Flexible Business Model

One of the most critical elements of becoming investment-ready is showing investors that you have a solid grasp of your business's financial risks.

While investors expect a level of risk, they want to see that your business model is adaptable enough to mitigate those risks effectively. This is where an experienced fractional CFO becomes invaluable. By continually assessing the profitability and sustainability of your business’s core metrics—such as the Unit of Economics (UoE)—they can identify potential weaknesses early and work with the wider team to address them.

A great example is when our team at Quantro identified that a client’s existing Unit of Economics (UoE) was neither sustainable nor scalable.

We worked closely with the client to adjust their pricing model and operational processes to address this. These changes successfully improved their UoE, ensuring it was profitable at scale.

Investors are drawn to this adaptability because it demonstrates that the business can pivot when needed, maintaining profitability while pursuing growth. This flexibility not only reduces perceived risks but also significantly increases investor confidence.

Aligning Finance with Management’s Vision for Consistency

A cohesive partnership between the finance team and the wider management is crucial for being investment-ready.

Investors want to see that there is alignment across the business, not only in terms of goals but also in the financial planning and strategy that supports those goals. Your finance team is the central hub that connects the various departments—whether it’s marketing, operations, or sales—ensuring everyone is on the same page.

This alignment is essential, especially when preparing governance structures, reports, and financial statements that will be presented to investors.

At Quantro, we always stress the importance of clear and constant communication between finance and management teams. The finance team or fractional CFO for small businesses not ready to have in-house full time CFO should understand the business inside out, from the strategic objectives to the key performance indicators (KPIs) that drive daily operations.

This allows the finance team to prioritise and suggest relevant financial reports that reflect progress towards the company’s goals. This level of integration ensures that when it’s time to sit down with investors, the business is able to present a unified and well-organised vision with financial data backing up the narrative.

Preparing for Investor Scrutiny with Organised Due Diligence

One of the key steps in being investment-ready is ensuring you’re prepared for the due diligence process.

Investors, while excited about the potential, are naturally cautious and will scrutinise the finer details of your business’s financial health before committing.

The faster and more organised your response to this scrutiny, the more confidence you will inspire. This is where the financial expertise of a fractional CFO comes in handy, ensuring that all financial documents are readily accessible and up-to-date, creating an organised “data room” that accelerates the process.

Simple but useful data room

At Quantro, we’ve found that having a well-prepared data room with financial statements from the past three years, a breakdown of assets and liabilities, and clear documentation of the company’s growth trajectory makes a significant difference.

Investors don’t want to hunt for information or be left waiting for key documents. When your finance team can present this information promptly and transparently, it shows that the business is not only investment-ready but also fully aware of its financial standing.

This level of preparedness signals to investors that your business operates with high professionalism and accountability, increasing their trust in your ability to manage the investment effectively.

Using Financial Insights to Tell a Compelling Growth Story

Numbers alone don’t tell the full story, but when used effectively, they can paint a vivid picture of your business’s growth potential. Investors want more than just raw data—they want to understand the narrative behind the numbers, and this is where your finance team plays a vital role.

By interpreting financial insights and aligning them with your broader business strategy, your finance team helps you communicate where your business stands and where it’s headed.

Dashboard always help tell a story

A good finance team or a fractional CFO knows how to weave a story around the numbers, making the data relatable and illustrating how it supports the business’s competitive advantage and scalability.

For example, rather than simply presenting revenue projections, your team can explain the rationale behind those figures—highlighting market demand, customer acquisition strategies, and operational efficiencies that make growth achievable.

This ability to blend data with storytelling reassures investors that your business is financially sound and poised for long-term success. Professionalism in presenting well-organised financials, combined with a compelling growth narrative, often sets businesses apart in the eyes of investors.

Anticipating and Addressing Investor Concerns

Investors will inevitably have questions and concerns about your business, no matter how promising it appears. What distinguishes a truly investment-ready business is its ability to anticipate and proactively address these concerns. The financial expertise of a fractional CFO plays a central role in this process by preparing answers backed by solid data and analysis.

Typical investor concerns range from revenue sustainability to operational risks, and a finance professional can help mitigate these financial challenges by providing clear, concise answers rooted in financial transparency.

A key aspect of managing investor concerns is demonstrating a strong understanding of potential risks and outlining how the business plans to manage them.

For example, investors may question how the business will remain profitable under different market conditions or how operational costs will be controlled as the company scales. You can address these concerns by presenting well-prepared financial models that explore scenarios backed by historical data and credible forecasts. This reassures investors that you have a firm grasp of the business’s future and highlights your proactive approach to risk management.

Continuous Communication and Alignment within the Team

Internal communication is key when preparing for investment, and your finance team is critical in ensuring everyone is on the same page. As the business goes through the fundraising process, different departments will naturally have questions and concerns about how the investment will impact them.

This is where financial professionals act as a vital link, keeping both the management team and broader business aligned on the financial strategy, goals, and milestones associated with the investment.

Maintaining open lines of communication is especially important during key phases of fundraising. The finance team can help set expectations internally, ensuring that employees understand the positive impact of investment while addressing any concerns about how it may affect operations.

Consistent communication also helps avoid disconnects between the company’s financial strategy and day-to-day activities, ensuring everyone works toward the same goals. Whether updating management on financial performance, providing insights into cash flow, or aligning with marketing and sales on budget expectations, a well-communicated financial plan builds confidence across the entire team.

Creating a Support System with Financial Advisors

While your internal finance team plays a critical role in preparing for investment, building a support system with external financial advisors or fractional CFO companies can add expertise and guidance to strengthen your investment readiness.

Fractional CFOs offer a fresh perspective, often identifying gaps or risks that may not be apparent within the organisation. Their experience in navigating the complexities of fundraising, understanding investor expectations, and refining financial strategies can help fill any gaps in your internal team’s expertise.

However, selecting the right fractional CFOs is key. They should complement the strengths of your existing finance team and offer specialised knowledge where needed—whether that’s in financial modelling, valuation, or legal compliance.

Building strong relationships with these advisors ensures that your business benefits from well-rounded guidance during fundraising. This external input can also be invaluable when tailoring your pitch decks to specific investors, as fractional CFOs often have extensive experience in what particular types of investors are looking for regarding data, reporting, and growth strategies.

This level of external support, combined with a strong internal finance team, allows you to approach raising capital confidently, knowing that all aspects of your financial health and financial management have been considered and optimised.

Ensuring Scalability and Sustainability in the Long Term

A critical part of being investment-ready is demonstrating that your business has the potential to achieve growth and sustain that growth over time. Investors are particularly interested in scalability—how easily your business can expand while maintaining efficiency and profitability.

Your finance team is crucial in building and communicating a scalable financial model using technological advancements. They ensure that operational costs, revenue streams, and cash flow management are all designed to support growth without stretching resources too thin.

Scalability doesn’t just involve cutting costs or increasing sales—it’s about having the systems, or implement systems and processes, and financial infrastructure to handle rapid growth. Whether it’s automating key processes, streamlining operations, or ensuring that the business can handle the increased demand for fast decision making, your finance team’s insight into resource allocation and cost control is invaluable.

By presenting a clear plan for how your business will scale and remain sustainable, your fractional CFO or an experienced in-house Chief Financial Officer can help you convince investors that their funds will be well-spent on long-term, profitable growth. This final layer of assurance often solidifies investor confidence, positioning your business as a viable candidate for raising capital.

Conclusion

Becoming investment-ready is not just about having a strong product or market potential; it’s about proving that your business is built on a solid financial foundation.

By leveraging financial professionals like fractional CFOs, part time CFOs or full time CFO, you can give investors the confidence they need to believe in your business’s future.

From crafting credible financial reporting and forecasts and addressing risks to ensuring alignment between finance and management and preparing for investor scrutiny with well-organised due diligence, your finance professionals play a pivotal role in this journey.

It’s also about the story your numbers tell—financial insights should reflect where your business is and where it’s going. You can confidently approach the fundraising process by demonstrating scalability and sustainability and having a clear support system that includes both internal and external financial experts.

Ultimately, a prepared and well-supported business increases the likelihood of securing investment, ensuring that your growth goals are achievable and sustainable in the long term.

Financial management can be daunting for many professional services businesses, but it's necessary. It often takes a backseat to client work and day-to-day operations. This is the old-fashioned way, and we often talked that finance should be at the heart of every business.

As neglecting financial clarity can lead to decisions based on gut feelings rather than solid data, potentially jeopardising the business's future. Streamlining financial reporting and analysis can unlock significant value, transform decision-making processes, and drive strategic growth.

There are common challenges businesses face when managing their finances. Still, the transformative power of data-driven decision-making and the crucial role of technology in modern financial management can help you overcome those.

Looking ahead to the future of financial reporting, the innovations in this field can offer businesses a competitive edge. Whether you're a founder looking to gain better control over your finances or a seasoned financial professional aiming to optimise your processes, understanding the impact of financial clarity on your business is key to long-term success.

The Challenges of Traditional Financial Management

In many professional services businesses, financial management and financial reporting is often an afterthought. Founders, especially those who focus on their craft rather than numbers, tend to overlook the importance of a robust financial strategy. This is absolutely normal, as the founders should focus on the business's growth.

This can stem from a lack of expertise in financial matters, insufficient time to focus on financial details, or simply not recognising the value that sound financial practices can bring to the business and can become a growth lever for your business.

As a result, decisions are frequently made based on gut instincts rather than hard data. While intuition has its business place, relying on it exclusively can lead to significant financial missteps. When financial clarity is absent, the business may face issues such as unmonitored spending, cash flow problems, and missed opportunities for growth.

The risks of operating without financial clarity cannot be overstated. Making decisions without reliable financial data can result in pursuing unprofitable ventures, misallocating resources, or failing to anticipate financial downturns.

Practical Example

For example, a company might decide to expand its services or hire additional staff based on perceived growth without realising that its cash reserves are dwindling or its margins are shrinking. This lack of financial insight can lead to decisions that, rather than propelling the business forward, create additional challenges and strain on resources.

To avoid these pitfalls, founders and business leaders must prioritise financial management from the outset by educating themselves, automating basic financial tasks, or engaging external experts to handle financial reporting and analysis.

The Power of Data-Driven Decision Making

The transition from instinct-based to data-driven decision-making can be transformative for a business.

This shift empowers leaders to make informed choices backed by tangible insights rather than gut feelings. One of the most significant advantages of data-driven decisions is identifying and addressing issues before they become major problems.

For instance, consider a scenario where a company's revenue remains stagnant over several months while its expenses steadily rise. This trend might go unnoticed without proper financial reporting until it significantly impacts profitability.

However, with streamlined financial analysis, such discrepancies can be identified early, allowing for timely interventions.

Practical Example

A real-world example of this can be seen in a client case where the absence of structured financial processes led to uncontrolled spending on freelance contractors. The company was hiring freelancers on an ad-hoc basis without benchmarking costs or implementing approval processes.

As a result, their expenses ballooned while revenue growth remained flat. Upon introducing regular financial reporting and analysis, the company was able to pinpoint this issue.

By implementing approval processes and conducting market research to find cost-effective freelancers, they reduced expenses and ultimately increased their bottom line by 289%. This example underscores the importance of using data to inform business decisions, leading to better financial outcomes and sustainable growth.

Ensuring Data Integrity: The Backbone of Accurate Financial Reports

Accurate financial reporting is only as good as the data it's based on. The phrase "garbage in, garbage out" perfectly encapsulates the importance of data integrity in financial management.

If the underlying data is flawed, any analysis, reporting, or decisions based on that data will be equally flawed, potentially leading to costly mistakes. Maintaining high-quality data is crucial for services businesses, where decisions are often made quickly and must be based on precise information.

Importance of bookkeeping

The foundation of accurate data often begins with solid bookkeeping practices. Ensuring that all financial transactions are recorded accurately and consistently allows businesses to maintain a clear and current view of their financial health. Regular audits and reconciliations are also essential to catch any discrepancies early.

Furthermore, businesses should invest in training their staff on the importance of data accuracy, ensuring that everyone involved in the data entry process understands the impact of their work on the company's overall financial strategy.

That is important not only for the finance department but for the business as a whole. As the world moves more into data, all businesses have started being data-driven. Therefore, training your people on the importance of data accuracy is important.

By prioritising data integrity, businesses can build a reliable financial reporting system that supports sound decision-making and long-term success.

The Role of Technology in Streamlining Financial Processes

Nowadays, technology plays an indispensable role in transforming financial reporting and analysis. Automation and cloud-based solutions have revolutionised how businesses manage their finances, making maintaining up-to-date and accurate financial data easier.

These tools help businesses reduce the time spent on manual data entry, minimise errors, and ensure that financial reports are generated swiftly and accurately. Automating repetitive tasks allows businesses to free up valuable time for more strategic activities, such as financial planning and analysis.

Practical example

When I first started working with a client, I soon realised they missed invoicing. That was due to flaws in the operational system.

Very soon, we changed our approach, and we automated the processes using easy-to-use tools like Notion. When we automated the reminders and created a view that we could easily spot errors or uninvoiced amounts, that small automation significantly improved the business's cash flows and helped them improve the receivables.

Getting cash as soon as possible can really transform your business. You can easily reinvest that money and access opportunities that you might have missed because of bad receivables management.

Technology advantages in financial statements

One of the most significant advantages of these technologies is the ability to create dynamic, real-time dashboards that provide a comprehensive overview of a business’s financial performance at any given moment. These dashboards integrate data from various sources, offering a unified view that stakeholders across the organization can access.

practical example

This real-time visibility is crucial in a fast-paced business environment, where the ability to make quick, informed decisions can be the difference between seizing an opportunity and missing it.

For example, if a company notices a sudden spike in expenses on its dashboard, it can investigate and address the issue immediately rather than discovering it weeks later when it might be too late to take corrective action.

practical example

Among the most important KPIs and dashboards a services business should monitor are the utilisation rate, capacity per department/individual, and the Unit of Economics for the clients.

Utilisation Rate and Capacity

It is important to understand how hard your team is working and if you have the capacity to onboard another client or if you need to hire before you do.

In addition, it will show you how efficient your business operations are and if you utilise the maximum out of your only asset as a business, your people. In any case, you must allow your people around 10% -20 % of their time for administrative/holidays/sick/training.

Unit of Economics

You should always know the profitability of your clients, as there are cases in which big clients tend to be over-sourced, causing a hole in the bottom line despite paying big money. So effectively, you might increase your top line, but your bottom line might decrease. Not only might you lose money on the client, but you might also miss an opportunity to acquire a new, more profitable client.

That financial reporting process will allow you to take fast actions and either change the pricing for the loss-making clients or potentially replace them, protecting your future growth.

other advantages

Moreover, cloud-based financial tools enable businesses to store and access their financial data securely from anywhere, facilitating better collaboration among team members, regardless of physical location. This is particularly beneficial for businesses that operate across multiple locations or have a remote workforce.

These tools also ensure that all team members are working with the most current data, reducing the risk of errors caused by outdated information. By leveraging technology, businesses can streamline their financial processes and enhance their overall efficiency and responsiveness, which eventually improves their company's financial health.

Looking Ahead: The Future of Financial Reporting and Analysis

As technology continues to evolve, the future of financial reporting and analysis in the services business is poised to become even more integrated and insightful.

One of the most exciting trends is the increasing blend of automation and human expertise. While automation tools can handle the bulk of data processing and routine reporting tasks, the role of financial professionals will shift towards more strategic activities, such as financial planning, risk management, and growth strategy development. This synergy between technology and human insight will enable businesses to operate more efficiently and make smarter, data-driven decisions.

Looking forward, advancements in artificial intelligence (AI) and machine learning (ML) are set to transform financial reporting further. These technologies can analyse vast amounts of data quickly, identifying patterns and trends that might not be immediately apparent to human analysts.

For instance, AI could predict future financial trends based on historical data, helping businesses anticipate market shifts and adjust their strategies accordingly. Financial reporting and analysis tools use AI to create forecasts. That needs some scepticism because the past is not an indication of the future. This is exactly where a financial professional like Quantro comes in. To identify trends and industry standards, the tools and knowledge in the industry must be used to create a predictable model for the future.

Another key trend is the growing importance of real-time financial reporting. As businesses become more global and markets more dynamic, the ability to access up-to-the-minute financial data will be crucial. This will allow businesses to respond more swiftly to changes in the market, make informed decisions on the fly, and maintain a competitive edge. Cloud-based platforms and advanced analytics tools will continue to play a significant role in making real-time reporting accessible and reliable.

Final Thoughts

In summary, the future of financial reporting and analysis will be defined by integrating advanced technologies and human expertise. As these tools become more sophisticated, businesses that embrace them will be well-positioned to enhance their decision-making processes, improve their financial performance, and achieve sustainable growth. By staying ahead of these trends and continuously adapting their financial strategies, professional services businesses can unlock new opportunities and maintain their competitive edge in an increasingly data-driven world.

After a few years of market shifts (COVID-19, tech recession and AI), the ability to adapt financial strategies to industry dynamics is not just a skill but a necessity. This is where the role of a fractional CFO becomes pivotal. Fractional CFOs bring a wealth of expertise and an external perspective that can significantly enhance a company's financial agility. They are the navigators in the sea of market changes, guiding businesses through uncertainties with strategic foresight and practical wisdom.

We aim to delve into the crucial aspects and benefits of adapting financial strategies in response to industry dynamics, offering insights and practical advice for businesses looking to thrive amidst change. Focusing on understanding market dynamics, optimising cash flow, maintaining a balance between agility and stability, leveraging data for decision-making, and preparing for future market shifts, we explore strategies to help businesses stay competitive and resilient.

Understanding Market Dynamics

Market dynamics are crucial for fractional CFO services and businesses aiming to navigate the rapidly changing economic landscape. These dynamics, driven by the forces of demand and supply, directly influence pricing strategies, product availability, and competitive positioning. For fractional CFOs, grasping these concepts is not just beneficial but essential, enabling them to guide businesses through fluctuations with strategic agility and foresight.

The COVID-19 pandemic highlighted the importance of adaptability as industries like digital marketing saw drastic shifts in demand. We played a key role in swiftly adapting financial strategies to leverage new opportunities and manage challenges. This ability to pivot quickly, informed by a deep understanding of market dynamics, underscores the value of preparedness and strategic planning in today's volatile market environment.

Maintaining a proactive stance and employing predictive analysis, we help businesses anticipate market shifts, ensuring they're always ready to act on new opportunities or mitigate potential risks. This approach is vital for our companies to stay competitive and drive growth in an ever-evolving marketplace.

The Role of Cash Flow and ROI: A Concise Guide

Understanding cash flow and return on investment (ROI) is crucial for any business aiming to navigate the complexities of the financial landscape. From our experience, these are not just metrics but vital indicators of a company's operational health and strategic success.

ROI Importance

ROI measures the profitability of investments, guiding strategic decisions to ensure resources and capital are allocated effectively. Investments with high ROI that align with strategic goals and good payback periods are prioritised, balancing immediate returns with long-term growth.

Balancing Act

Achieving a balance between positive cash flow and high ROI requires a dynamic financial strategy. It's about being adaptable and making informed decisions that support both stability and growth.

Practical Tips from Fractional CFO

Monitor Cash Flow Regularly: Stay informed about your financial status to make timely adjustments.

Evaluate Investments for ROI and payback period: Choose investments that promise the best returns at the shortest possible period aligned with your business goals.

Stay Flexible: Adapt your financial strategies to market changes, focusing on immediate needs and future opportunities.

Leveraging cash flow and ROI effectively can guide your business towards sustainability and growth, emphasising the importance of strategic financial planning in today's dynamic market.

Achieving a Balance between Agility and Stability

Balancing agility and stability in financial planning is crucial for navigating the unpredictable business landscape. Our experience underscores the importance of this balance, allowing for swift adaptation to market changes while maintaining a solid financial foundation.

Agile planning involves regular updates to financial forecasts, enabling responsive decision-making based on current market conditions. Shifting from annual to more frequent, such as quarterly, forecasting has allowed us to allocate resources more efficiently and seize growth opportunities promptly. Also, our bespoke dynamic dashboard, with live updates, supports our businesses on strategy shifts from finance to operations.

Stability is achieved through strong financial controls and maintaining healthy cash reserves. These practices protect the business's financial health, supporting operational continuity and strategic initiatives even amidst market volatility.

The essence of striking the right balance lies in viewing agility and stability in-house, not as opposites but as complementary forces. This balanced approach is vital for sustained growth and effectively navigating market dynamics.

The interplay between financial expertise, agile planning and stable financial underpinnings forms the backbone of successful financial strategy adaptation in today's fast-evolving business environment.

Leveraging Data for Informed Decision-Making

Using data analytics is critical to adapting strategies effectively. Our experience has shown that data-driven insights greatly enhance decision-making, allowing rapid adjustments to meet market demands. Here, we explore the essentials of leveraging data for strategic advantage.

Dynamic Dashboards

Dynamic dashboards have provided real-time insights into financial and operational metrics. This visibility allows for swift strategic adjustments, ensuring decisions are based on the latest data.

Strategic Adjustments with Data

Analysing trends and forecasting enables us to anticipate market changes, proactively optimising our financial strategies. This approach leads to better investment decisions and operational efficiency, driving improved financial performance.

Cultivating Data Literacy

Promoting data literacy across the organisation amplifies the impact of data analytics. Providing training in skills and tools empowers team members to make evidence-based decisions, contributing to a more agile and informed decision-making process.

Data analytics transforms financial decision-making, offering a clear path through complex market dynamics. Businesses can navigate confidently by harnessing real-time insights and promoting data literacy, ensuring they stay competitive and ready for growth. Our journey highlights the value of a data-driven approach as a fundamental part of modern financial strategy.

Preparing for Future Market Shifts

Preparing for future market shifts is not just strategic—it's essential for survival and growth. Our experience has taught us the importance of anticipation and adaptability, enabling us to remain resilient through various market changes. This section provides insights into how small businesses also can prepare for and adapt to future market dynamics.

Anticipating Change with Market Research

Staying ahead of market shifts begins with robust market research. By continuously monitoring industry trends, customer behaviour, and technological advancements, we've been able to anticipate changes before they fully impact the market. This proactive stance allows for strategic planning and innovation, ensuring we're always a step ahead.

Building a Flexible Business Model

Flexibility in business operations and financial planning is key to navigating market shifts. We've learned the value of having adaptable processes and a diversified portfolio. This flexibility has enabled us to pivot quickly in response to changing market conditions, minimising risks and capitalising on new opportunities.

Continuous Learning and Innovation

Embracing a culture of continuous learning and innovation is vital. We've fostered a dynamic environment where adaptive strategies thrive by encouraging innovation and staying open to new ideas. This approach has helped us respond to immediate market changes and positioned us for long-term success.

The Path to Financial Resilience

Throughout this exploration into adapting financial strategies amidst shifting industry dynamics, we've highlighted key strategies: understanding market dynamics, prioritising cash flow and ROI over revenue first, achieving agility and stability, leveraging data for strategic decisions, and preparing for future market shifts. These elements are crucial for navigating today's unpredictable business landscape.

The overarching message is clear: adaptability is essential. Businesses that remain dynamic, informed, and forward-thinking in their financial planning are better equipped to thrive. Cultivating this adaptability requires dedication to strategic planning and an openness to continuous learning and innovation.

Success in the future market depends on a commitment to staying informed and embracing change; we at Quantro are committed to adapting our fractional CFO services to the market needs and each business's needs.

Starting a new business is a challenging journey. Managing cash flow effectively is one of the most critical hurdles for early-stage startups. According to CB Insights, running out of cash is one of the top reasons startups fail, highlighting the importance of robust cash management practices. This guide provides practical strategies and insights to help startup firms navigate the complexities of cash flow and cash equivalents, ensuring their business survives and thrives.

We will explore essential strategies for managing cash flow, including the benefits of automating cash-flow forecasting, the advantages of prepaid annual contracts, and the importance of maintaining a cash reserve fund.

We'll also discuss balancing cost-cutting with growth opportunities and explore innovative methods for securing early funding.

By implementing these strategies, startups can build a solid financial foundation, enabling them to focus on growth and innovation.

The Importance of Cash Flow ManagementUnderstanding Cash Flow

Cash flow is the lifeblood of any startup. It refers to moving money into and out of your business, encompassing all operational expenses (operating cash flow), investments, and income. Positive cash flow means your startup can meet its obligations, invest in growth opportunities, and cushion against unexpected downturns.

Conversely, negative cash flow can lead to insolvency, stunted growth, and business failure. Managing cash flow effectively ensures that your startup remains viable, providing the financial stability needed to weather early-stage challenges and capitalise on market opportunities.

Consequences of Poor Cash Management:

Startups are particularly vulnerable to cash flow issues due to their reliance on initial funding and often unpredictable revenue streams. Poor cash management can lead to severe consequences, including missed growth opportunities at best, inability to pay suppliers or employees, and damage to business relationships and credit ratings.

According to many studies around why startups fail, running out of cash is the second most common reason. Therefore, understanding and managing cash flow isn't just a financial task—it's a strategic imperative that can mean the difference between success and failure for an early-stage startup.

Automating Cash-Flow ForecastingThe Power of Automation

In the fast-paced environment of a startup, having a clear and real-time view of your financial health is crucial. Automating cash-flow forecasting can provide this clarity, significantly impacting financial management. For instance, by using tools, startups can gain real-time insights into their financial status. We like Google Sheets for automating cash flow forecasting because of its openness capabilities and creating live dashboards with alerts.

Other cash flow software can produce automated cash flow statements and everything related to cash, like the Float app, which connects directly to your accounting software. However, like every other tool, it has some limitations.

This automation allows for better decision-making, providing an accurate picture of when and where cash will enter and leave the business. As a result, startups can anticipate cash needs, avoid potential shortfalls, and manage their financial operations more efficiently.

Practical Implementation and Benefits

One of our clients struggled with cash flow management until we automated their cash flow in Google Sheets.

We set up a live dashboard with alerts, enabling them to handle their inventory more effectively and manage difficult cash situations in advance. When inventory dropped below a certain threshold, they received a notification to their Slack. It was the same with money; when cash dropped a certain threshold, they had a message in their Slack. Then, we followed up with strategies and useful tips to improve the situation.

This automation provided immediate efficiency in stock orders and allowed them to proactively plan for future financial needs.

Using such automated tools, startups can ensure they have sufficient cash to meet operational needs, invest in growth opportunities, and cover unexpected expenses.

Automating cash flow forecasting benefits include improved financial resilience, enhanced operational efficiency, and a stronger foundation for long-term success.

Utilising Prepaid Annual Contracts

Boosting Cash Flow with Prepaid Annual Contracts:

One effective strategy to improve cash flow is to use prepaid annual contracts.

This approach involves negotiating with customers to pay for a year’s worth of services upfront, providing an immediate influx of cash. This strategy is particularly beneficial for startups that do not have the luxury of abundant venture capital funding. By securing a full year's payment at once, startups can ensure they have sufficient funds to cover operational costs and invest in growth opportunities.

Bonus Tip

You can take advantage of credit cards that provide you with instalments. For example, you can pay your subscriptions annually for better payment terms, like 20% discounts. You can use a credit card to split the payment into 3,6,9, or 12 instalments with 3% internet.

That means you take the best out of both worlds, taking a huge discount on your subscription but not paying cash upfront because you will be split into the credit card platform for 12 months.

Overcoming Challenges in Negotiations:

Convincing customers to commit to prepaid annual contracts can be challenging, especially for smaller businesses.

However, providing incentives such as discounts for annual payments or enhanced customer support can make the offer more attractive.

In our experience, smaller businesses are often open to paying upfront if they see the value and security in their investment. This strategy stabilises cash flow and fosters stronger customer relationships by demonstrating confidence in the value provided.

Maintaining a Cash-Reserves Fund

Importance of Cash Reserves:

Establishing and maintaining a cash reserve fund is essential for the financial stability of an early-stage startup.

A cash reserve fund acts as a safety net, providing a buffer against unexpected expenses or periods of reduced income. Ideally, this fund should be large enough to cover at least three months’ operating expenses.

This financial cushion ensures that the business can continue to operate smoothly even when faced with unforeseen challenges, such as delayed payments from clients or sudden drops in revenue.

Bonus Tip

Utilise that cash reserve fund in investing activities like next-day liquidity accounts or dividend accounts, and you will get around 5% interest on idle cash.

Building and Managing the Fund:

To build a cash reserve fund, startups should adopt disciplined saving practices and strategic financial planning.

One effective technique is to set aside a portion of monthly profits into a separate, interest-bearing account.

Utilising financial products like cashback credit cards can also help accumulate additional funds. It’s important to get into the mindset that these reserves are for emergencies only and not to be used for day-to-day operations (net cash flow). By treating this fund as an untouchable reserve, startups can ensure they are prepared for financial uncertainties while maintaining a strong operational footing.

Deciding Between Cutting Costs and Investing in Growth

Balancing Act: Cost-Cutting vs. Growth Investment

One of the most critical decisions for startup founders in young companies is determining when to cut costs and invest in growth opportunities.

Running a lean operation is essential, particularly in the early stages, to avoid unnecessary expenditures that can drain your cash reserves.

However, it is equally important to identify and seize growth opportunities that offer a high return on investment (ROI). The key is to assess each expense and potential investment through the lens of ROI, ensuring that every dollar spent contributes meaningfully to the company's growth and sustainability.

Evaluating Costs and Opportunities:

Startups should regularly review their financial statements to identify non-essential expenses that can be eliminated without compromising core operations.

This might include downsizing office space, renegotiating supplier contracts, or reducing discretionary spending. On the flip side, evaluating growth opportunities involves analysing their potential impact on revenue and scalability.

For example, investing in a marketing campaign that has historically shown a high conversion rate or developing a new product feature that meets customer demand can drive substantial growth. The decision-making process should be data-driven, prioritising investments with the highest potential ROI while maintaining financial prudence.

Securing Early Funding

Exploring Funding Options

Securing early funding is vital for startups to build a solid financial foundation and fuel their growth. Traditional funding sources, such as bank loans, are often challenging for startups due to the high risk associated with new ventures.

However, various alternative funding options can provide the necessary capital without the stringent requirements of traditional loans. These include venture capitalists, angel investors, and innovative methods like factoring invoicing, which involves selling your accounts receivable at a discount to get immediate cash.

Innovative Approaches and Considerations:

Another practical approach is utilising credit facilities or credit cards that offer instalment plans or buy-now-pay-later options, providing flexibility in managing cash flow.

Cashback credit cards can also be beneficial by offering returns on expenditures, which can be funnelled back into the business. It’s crucial to carefully evaluate the costs and fees associated with each funding option to ensure it aligns with your financial strategy and operational needs.

Maintaining strong relationships with investors and exploring creative financing methods can give startups the liquidity to navigate the early stages and drive sustainable growth.

Conclusion

Recap of Key Points

Managing cash and cash equivalents effectively is crucial for the survival and growth of early-stage startups. By automating cash-flow forecasting, startups can gain real-time insights and make informed financial decisions. Using prepaid annual contracts can provide an immediate cash influx, helping stabilise finances.

Maintaining a robust cash-reserves fund ensures the business can weather unexpected financial challenges.

Balancing cost-cutting with growth investments requires careful ROI analysis, ensuring that every expenditure contributes meaningfully to the company’s objectives.

Finally, exploring various funding options, from venture capital to innovative financing methods, can provide the necessary liquidity to support startup growth.

Final Thoughts:

Navigating a startup's financial landscape is no easy task, but it is possible to build a solid financial foundation with the right strategies and tools. Proactive cash management ensures operational stability and positions the startup for sustainable growth and success. By implementing the strategies discussed in this guide, startup founders can better manage their cash flow, make strategic investments, and secure the funding needed to drive their business forward.

For further guidance and resources, consider consulting with financial experts, leveraging financial management tools, and continuously educating yourself on best practices in cash management.

Your startup’s success depends on your ability to navigate these financial challenges effectively. Start implementing these strategies today to secure a brighter future for your business.

Business loans and financing options can be daunting for many entrepreneurs and small business owners. A business loan is one of the key financing options available, offering various terms and types tailored to meet the unique needs of different businesses. There are numerous tools out there and many financing options; understanding how to utilise these financial tools effectively is crucial to sustaining operations and achieving growth and innovation. Choosing the wrong business loan can plummet the company instead of lead to growth. So, the process with a clear pathway is important to navigate the financing landscape, focusing on both traditional and creative approaches to securing your business's funds.

Business financing is not just about getting the capital to start or expand your business; it’s about strategically choosing and utilising financing options that align with your company’s long-term goals. Whether you’re considering a standard bank business loan, exploring government-backed loans, or looking into more innovative solutions like invoice factoring, flexing payables or even credit card instalments, each option comes with its own set of benefits and challenges. So, choose wisely which financing option is right for you, which will become a lever growth instead of a growth blocker.

Understanding Your Business Loan Application and Financing Needs

Before exploring the diverse range of financial products available, it’s crucial for business owners, sole traders, or limited companies to identify why they need financing.

This understanding shapes the approach to selecting the right financial tool tailored to specific business demands. For instance, a long-term loan with a lower interest rate might be ideal for expansion. Considering the annual interest rate (AIR) and the annual percentage rate (APR) is essential when choosing a loan for long-term financing, as these rates determine the total cost of credit and the actual yearly cost of borrowing over the loan term.

However, if bridging a short-term cash flow gap is the goal, a quicker solution like invoice financing or a line of credit could be more appropriate. This strategic alignment of financial needs with the correct financing type is fundamental to avoid overborrowing or underutilising funds, which can hamper financial health in the long run. The efficiency of the business loan application process and its quick disbursement of funds upon approval are crucial in aligning with these financial needs.