Working capital is one of those areas every business depends on, yet most founders rarely look at closely. They focus on their P&L, celebrate revenue wins and push for growth, while the Balance Sheet sits quietly in the background. The problem is that profit does not keep a business alive. Cash does. You can have healthy sales, strong margins and a confident forecast, yet still find yourself unable to pay suppliers or meet payroll on time. It is a contradiction that catches out even the most promising companies.

The truth is simple. Businesses do not fail because they are unprofitable, they fail because they run out of cash. We see this often. Founders chase growth, sign new clients and expand their teams, but forget to ask when the cash from this activity will arrive. They allow invoices to drift, pay expenses earlier than needed or increase their cost base before their cash position can support it. On paper they look successful, but underneath, liquidity is tightening. Working capital becomes the silent pressure point in the business, the place where good intentions meet financial reality.

When working capital is understood and managed properly, everything changes. It gives leadership the clarity to grow with confidence and the control to protect the business during periods of uncertainty. It turns profit into usable fuel rather than a number on a report. Done well, working capital management stops being a technical exercise and becomes the foundation for sustainable, cash centred decision-making. It is not just about improving processes. It is about helping founders build a business that succeeds not only on paper, but in practice.

Why Founders Overlook Working Capital

Most founders are naturally drawn to the P&L. It is the document that shows growth, momentum and commercial success. It is where revenue targets live and where performance is judged. The Balance Sheet, by comparison, can feel static and less urgent. Yet this focus on top-line progress often hides the real issues. A company can be growing quickly, winning new customers and increasing its margins, while at the same time building a hidden cash problem that only becomes visible when it is too late.

The most common reason this happens is a lack of visibility. Many founders simply do not know what they are owed or what they owe at any point in time. They underestimate how much capital is trapped in overdue invoices, early payments or expanding cost bases. Without a clear picture of accounts receivable and accounts payable, decisions are made on optimism rather than on available liquidity. The result is a business that appears healthy on paper but is stretched in practice.

At Quantro we see this pattern again and again. The issue is rarely that a company is unprofitable. It is that cash is being managed on guesswork. Once founders begin to look beyond the P and L and understand the timing and movement of cash within the business, the picture becomes clearer. Working capital shifts from being an afterthought to becoming a core part of strategic planning. The companies that make this shift are the ones that grow sustainably rather than dangerously.

The Two Working Capital Levers That Break First

When a business begins to grow, the first cracks rarely appear in revenue or profit. They show up in accounts receivable and accounts payable. These two levers determine how cash moves through the business, yet they are often the least understood by founders. Accounts receivable is where cash becomes trapped. It represents work completed and revenue earned, but not money in the bank. When invoices are allowed to drift or credit terms extend beyond what the business can comfortably support, liquidity tightens long before it shows up in the P&L. This is why understanding the core working capital metrics becomes essential. They reveal whether your business has the immediate financial strength to operate and how efficiently cash moves through its daily cycle.

At the foundation sits the Current Ratio, a straightforward test of short term health. It is calculated as Current Assets divided by Current Liabilities. Current assets are items the business expects to convert into cash within twelve months, such as cash itself, accounts receivable and inventory. Current liabilities are obligations due within the same period, such as supplier invoices, short term loans and tax payments. A ratio above one suggests the business can cover its short term commitments, while a ratio below one can signal potential strain. Working Capital expresses this same relationship in absolute terms, calculated as Current Assets minus Current Liabilities. For example, if a company has current assets of 450,000 pounds and current liabilities of 300,000 pounds, its working capital is 150,000 pounds. These fundamentals provide a financial safety check, but they only tell part of the story.

The deeper insight comes from understanding the timing of cash. This is where operational KPIs matter. The Cash Conversion Cycle shows how long cash is tied up in operations before it returns to the bank account. It is calculated as Days Sales Outstanding plus Days Inventory Outstanding minus Days Payable Outstanding. Days Sales Outstanding measures how quickly customers pay. Days Inventory Outstanding measures how long stock sits before it is sold. Days Payable Outstanding measures how long the business takes to pay suppliers. When these measures are monitored together, they reveal how efficiently the business turns activity into cash and where delays are building. A rising cycle is an early warning that cash is becoming stretched, even if profit looks healthy. This is why these KPIs are central to diagnosing working capital pressure early, rather than reacting once the problem appears on the P&L.

Accounts payable tells a similar story from the opposite direction. Many businesses pay suppliers earlier than necessary, either out of habit or in a well intentioned attempt to maintain strong relationships. The intention may be positive, but the outcome is often damaging. Cash leaves the business faster than it needs to, reducing the breathing room required to operate with confidence. When accounts receivable slows and accounts payable accelerates, even profitable companies begin to feel the strain. Understanding DPO gives founders the clarity to set payment timings that support cash flow without harming supplier relationships.

At Quantro we see this pattern in nearly every client we support. The problem is rarely that the business model is broken. It is that founders lack visibility of what they are owed and what they owe at any point in time. By implementing real time cash flow tools and weekly dynamic accounts payable reports, we help founders see the movement of cash clearly and act on it quickly. Once these two levers are understood and managed with intention, the business begins to operate on solid ground rather than on hope.

The Outdated View of Working Capital and Why It Hurts Businesses

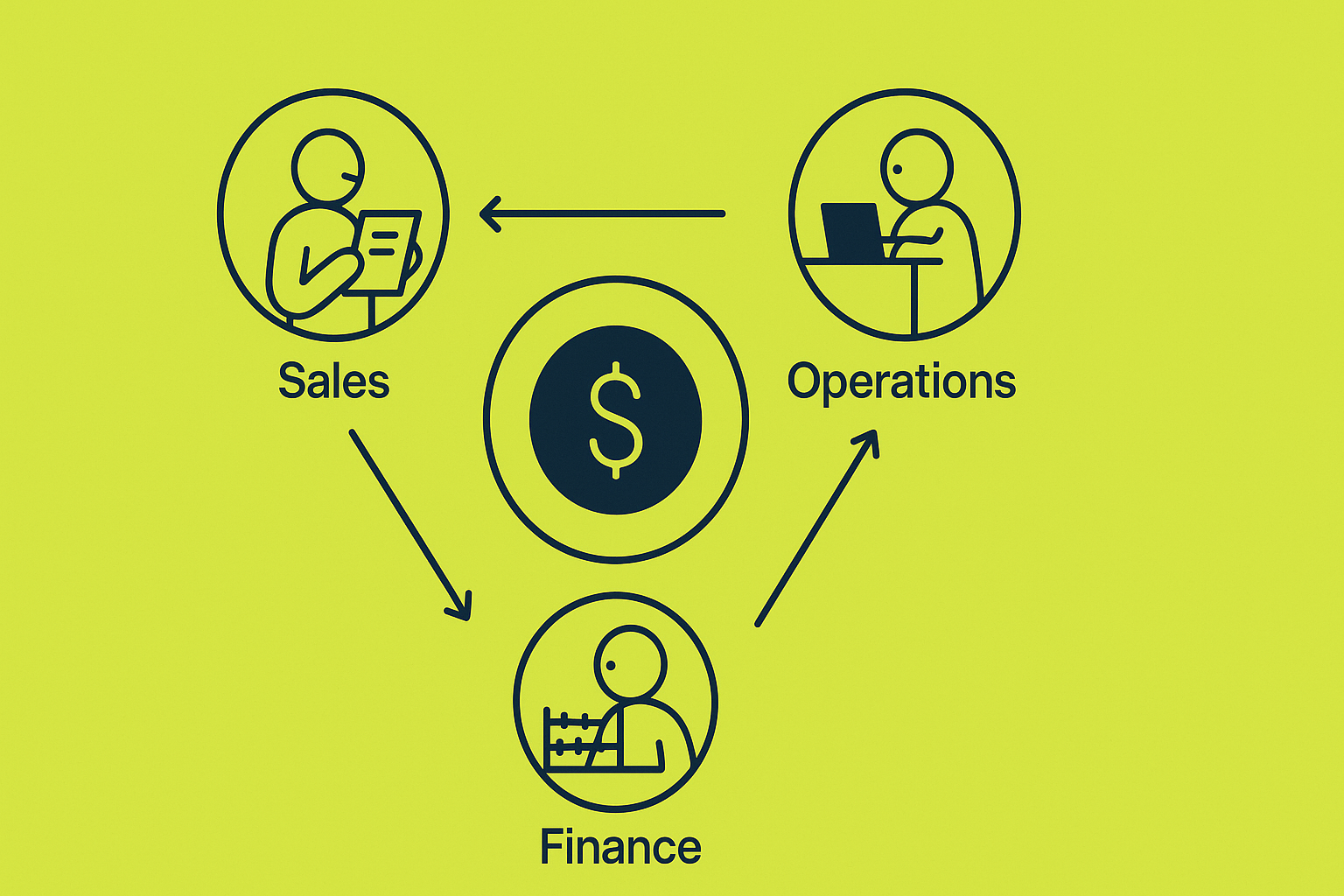

For many companies, working capital is still treated as a technical chore rather than a strategic advantage. It sits in the background of the finance function, managed quietly through invoicing routines, supplier cycles and basic reconciliation. This narrow view assumes that working capital is simply an administrative process: collect what is owed, pay what is due and keep everything moving. The problem is that this approach misses the bigger opportunity. It separates day to day cash management from the decisions that shape the future of the business.

When working capital is viewed in isolation, it is easy for teams to optimise their own priorities without considering the wider impact. Sales teams focus on closing deals regardless of payment terms. Operations push for efficiency without considering stock levels or supplier timing. Finance tries to manage the consequences rather than drive the strategy. Each department operates with good intent, yet the combined effect can quietly weaken liquidity. A business can look efficient on paper while unknowingly tightening its own cash position.

A more modern view brings working capital into the centre of strategic planning. Payment terms become a competitive tool, not an afterthought. Inventory management becomes a lever for resilience, not only for efficiency. Cash timing becomes part of every investment discussion, from hiring to marketing. At Quantro we encourage founders to treat working capital as an active management discipline. When it is integrated into everyday decision making, the business becomes more predictable, more resilient and far better prepared for growth.

This is also the point where the right metrics begin to matter. The Current Ratio and the absolute working capital number provide a snapshot of short term strength, while measures such as Days Sales Outstanding, Days Payable Outstanding and Days Inventory Outstanding reveal how quickly cash moves through the business. The Cash Conversion Cycle brings these elements together to show how long it takes to turn investment back into cash. Working capital turnover and the Quick Ratio can add further clarity. When founders track these indicators consistently, they gain a far deeper understanding of liquidity and can make decisions with greater confidence.

Helping Founders Understand the Profit and Cash Divide

For many founders, the hardest shift is accepting that profit and cash do not move at the same pace. Profit shows the outcome of the work the business has done. Cash shows whether the business can actually afford to keep going. When these two are out of sync, even healthy companies begin to feel pressure. We often find that once founders see the timing difference between when revenue is earned and when it is collected, the entire financial picture changes for them. It becomes clear that the problem is not growth, but the rhythm of cash flowing through the business.

Our role at Quantro is to make this divide visible and understandable. We strip away unnecessary complexity and highlight the points where cash is delayed or released. This creates space for better decisions. Founders can see precisely how long it takes to turn a sale into usable cash and how each payment cycle affects liquidity. When this understanding is embedded into regular discussions, the business becomes more proactive. Cash stops being a surprise and becomes part of everyday planning.

What makes this approach powerful is that it replaces assumptions with clarity. Instead of chasing revenue in the hope that cash will follow, founders begin to manage their business with a clearer sense of timing and control. They understand that a company can be profitable and still vulnerable if cash is not managed with discipline. Once the distinction becomes part of the culture, decisions become steadier, planning becomes sharper and the business gains the resilience it needs to grow with confidence.

Turning Working Capital into Confidence

Working capital is not a background task or a technical detail. It is the financial heartbeat of a business, and when it is ignored, even the most promising companies can find themselves under pressure. The difference between profit and cash becomes painfully clear when invoices are slow, expenses mount and the timing of money in and money out drifts out of sync. Yet the opposite is also true. When working capital is managed with intention, businesses gain stability, resilience and the freedom to grow on their own terms.

What we see at Quantro is that the moment founders understand the movement of cash in their business, everything becomes clearer. Decisions feel less reactive, planning becomes more grounded and growth becomes something that feels controlled rather than chaotic. Cash stops being the thing that surprises you and becomes the thing that supports you. This shift is not theoretical, it is practical. It is the difference between a business that survives and one that grows with confidence.

If you are ready to turn your working capital into a tool for growth rather than a source of stress, we would love to help. Book a meeting with our team to explore how Quantro can build a working capital structure tailored to your business. One that gives you not just profit, but clarity, control and confidence.